Rising mortgage rates unlikely to dampen property demand in Singapore until they climb above 3pc, say analysts

[ad_1]

SINGAPORE, July 25 — The modern lender hikes on home finance loan prices are not likely to dampen desire for both of those public and private attributes except the prices edge previous 3 for each cent, numerous property analysts reported. For now, this intended that residence charges will continue to soar.

They were commenting on the second quarter residential assets transactions data produced on Friday (July 22) by the Housing and Growth Board (HDB) and Urban Redevelopment Authority (URA).

In April to June this year, there have been 6,819 resale transactions for public flats, a 1.7 for each cent decrease from the 6,934 transactions recorded in the past quarter.

Meanwhile, resale price ranges for public homes rose 2.8 per cent from the prior quarter, which is marginally larger than the 2.6 for every cent in flash estimates supplied by HDB previously this thirty day period.

The resale value index, which presents facts on the typical selling price actions in the resale community housing current market, was 163.9 in the next quarter — an increase from 159.5 in the earlier quarter.

As for private properties, rates rose at a a lot quicker tempo of 3.5 for every cent in the next quarter of this calendar year, 5 occasions the .7 for each cent enhance in the previous quarter.

The private household home rate index greater to 180.9 in the second quarter, up from 174.8 in the previous a few months, in accordance to URA’s facts.

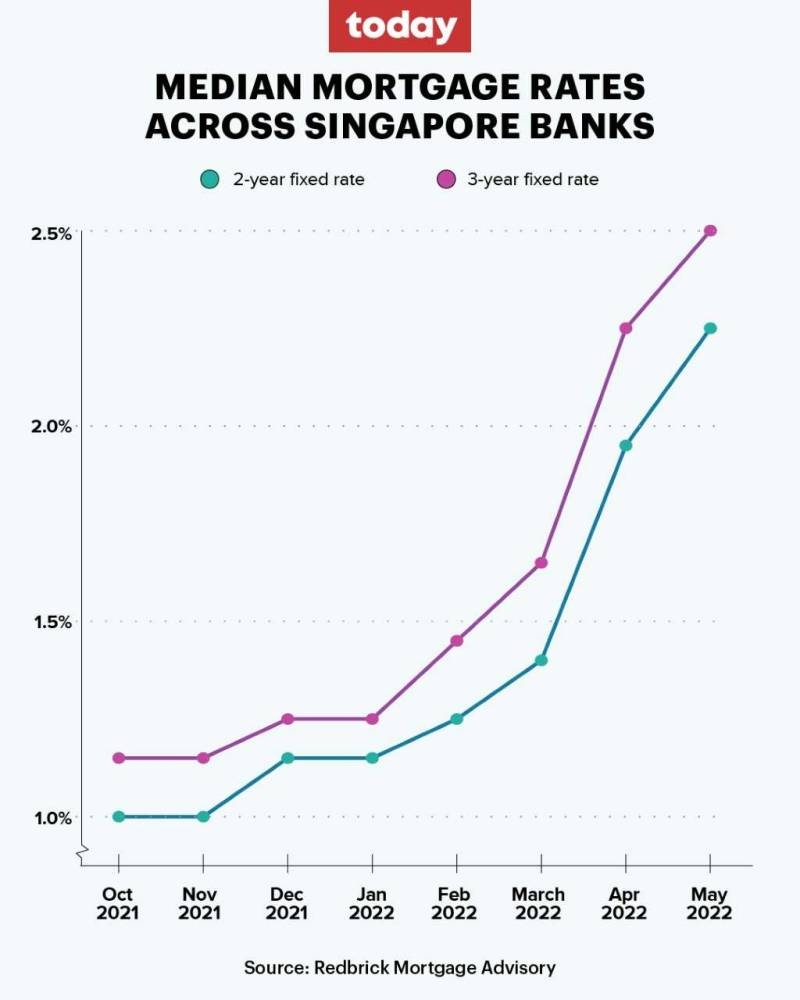

In basic, two-calendar year and 3-12 months house loan loans which carry a preset fee have noticed median charges go up from about 1.5 for every cent at the start of the yr to additional than 2.6 for each cent, according to a CNA short article final thirty day period.

As of Friday, the fastened rates for two-year home personal loan deals at DBS lender and OCBC are 2.75 per cent and 2.98 for each cent respectively

Nonetheless workable, for now

With median mortgage prices climbing, banking companies and house specialists before warned homebuyers to set apart adequate cost savings as a “buffer” and to search for new personal loan deals or preparations if essential.

Despite this, Huttons Asia’s senior director for research Lee Sze Teck instructed Today that he does not believe the climbing fascination rates on mortgages will influence demand from customers for housing in normal.

Altitude Serious Estate’s important executive officer Nelson Lim added that “there is always a market” for authentic prospective buyers who require a home to are living in instead than invest in.

Climbing curiosity prices, he stated, will only temper a buyer’s anticipations of the sort of household they can order and the amount of money of funds they can borrow.

“By and huge…even however there is an boost in the curiosity charges, it is however reasonably priced at this position,” reported Lim. “So I do not see curiosity premiums as staying a very big deterrence for people today obtaining assets.” Agreeing, Christine Sunlight, senior vice president of research and analytics at OrangeTee and Tie, reported the fascination charge hike has not afflicted the community housing resale market considerably, as the personal loan quantum of most HDB flats is not superior, and most property owners are not about-leveraged.

As for the personal residential assets industry, she reported most current owners need to be able to services their dwelling loans now

The 3computer threshold

Nevertheless, the climbing desire rates supplied by banking companies for home mortgages are extra probably to be keenly felt when they edge previous the 3 per cent mark, said the analysts.

Pointing out that the whole debt servicing ratio (TDSR) threshold for residence financial loans uses a stringent 3.5 for each cent desire charge computation, Sunshine stated there ought to be ample buffer for charges to go right before month to month house loan obligations exceed borrowers’ gross monthly revenue.

This would mean that the price of borrowing will make any difference far more for home consumers, which could impact their conclusion on how a great deal to spend on a household obtain, or irrespective of whether to purchase 1 in the initially location.

The TDSR refers to the portion of a borrower’s gross every month profits that goes toward repaying the month-to-month personal debt obligations, like the financial loan staying used for.

In a bid to interesting the housing sector, the TDSR was decreased from 60 per cent to 55 for every cent very last December. This indicates that a person’s full regular monthly mortgage payments, together with house loan financial loans, are unable to exceed 55 for every cent of his or her total gross revenue.

Sunshine stated should really this kind of a scenario occur, far more initially-time debtors may switch to an HDB mortgage pegged to 2.6 for each cent, or paying out down their financial loans to lessen their month-to-month instalment, if they are in the community housing resale sector.

Wong Siew Ying, head of investigate and information at PropNex Realty also explained that some potential buyers who ended up beforehand eyeing personal residential houses “may come to a decision to play it safe and sound and choose to acquire a resale flat, which is generally much more economical as opposed to a non-public condominium.

Altitude Real Estate’s Lim added that mentioned purchasers will only probable begin performing their “calculations” as soon as the fascination charges go over and above 5 for every cent mainly because it will affect their disposable earnings.

Nevertheless, he was optimistic that individuals who genuinely require a home will be in a position to afford a single if the fascination costs stay in the 5 for each cent selection.

But they may perhaps be additional restrained when it arrives to finding more substantial-sized houses, or those on better flooring, which price additional, he claimed.

Sturdy market place

Transferring ahead, the analysts expect both housing charges and the market place to continue to be solid.

They projected that the quantity of resale flats that will be transacted this year will be among the vary of 25,000 and 28,000, with resale charges for the rest of the 12 months growing in between 7 and 10 for every cent from 2021.

Said Sunlight: “As HDB proceeds to start a lot more BTO flats in the second fifty percent of this calendar year, the elevated housing offer will continue to draw demand from customers away from the resale industry, which may assist to control the rate of value expansion and tame marketplace exuberance.”

As for the private household properties, the analysts estimated that the prices of new homes, excluding executive condominiums, might increase by 6 to 9 for each cent this 12 months as as opposed with 2021, when all around 9,000 to 10,000 models may possibly be transacted.

Sunshine included that for the resale market place, rates in the complete of 2022 might raise by in between 6 and 8 for every cent from the previous 12 months, and about 11,000 to 13,000 resale residences could be sold.

“Amidst world headwinds, Singapore’s sturdy economic advancement and continually large employment rate may perhaps aid cushion house owners from the impression of the worldwide economic uncertainties,” explained Sun.

“Moreover, traders flocking to common save havens to preserve their cash may well nevertheless park their dollars right here as our house expense sector is deemed one of the most secure and most secure in the planet.” — These days

[ad_2]

Supply hyperlink