Construction purchasers report recovery losing momentum

[ad_1]

Study respondents pointed out that better charges and problems about the economic outlook experienced started off to act as a brake on need. Optimism about potential workloads slipped to its cheapest in far more than 18 months.

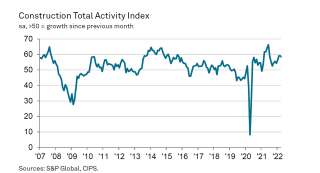

At 58.2 in April, down from 59.1 in March, the headline S&P World / CIPS United kingdom Development Buying Managers’ Index signalled the weakest price of output development considering that January. The index has nevertheless posted higher than the vital 50. no-change mark in each and every thirty day period given that February 2021.

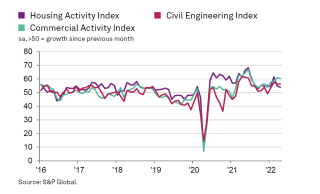

Of the 3 most important design segments monitored by the study, the swiftest-increasing remained commercial do the job (index at 60.5), followed by civil engineering (56.2). Household get the job done remained the worst-undertaking sub-sector in April and noticed the biggest decline of momentum (at 53.8, down from 54.9 in March).

Development firms cited pent up need and spending related to Covid-19 restoration strategies driving need for business tasks, while key infrastructure strategies such as HS2 and Hinkley Point C continue on to raise civil engineering action.

The near-phrase outlook for building exercise deteriorated in April as overall new order volumes expanded at the slowest amount for four months. Escalating raw product price ranges and, in some cases, hesitancy because of to better borrowing expenses and geopolitical uncertainty ended up reported as headwinds to demand from customers.

A robust pipeline of design jobs and initiatives to improve depleted stocks resulted in a steep increase in paying for activity. Better degrees of enter shopping for have been recorded in just about every thirty day period given that June 2020. But suppliers are nonetheless battling to hold up with need for design items and resources. All over 45% of the survey panel described longer lead situations, even though only 2% had witnessed any enhancement.

Offer chain delays were attributed to shortages of employees, components and transportation, with these complications frequently exacerbated by delays at ports and the war in Ukraine.

Higher rates paid out for energy, fuel and raw resources led to a steep raise in ordinary price burdens during April. Survey respondents also observed that the elimination of pink diesel subsidies had pushed up expenses. The over-all charge of acquiring rate inflation accelerated to its speediest since September 2021.

Searching in advance, 43% of development providers are forecasting an upturn in enterprise action through the following 12 months and only 12% are expecting a fall. Nevertheless, this gap is narrowing.

Tim Moore, economics director at S&P World-wide, which compiles the survey, said: “The construction sector is transferring toward a far more subdued restoration period as sharply soaring strength and uncooked material costs hit client budgets. Residence building saw the greatest loss of momentum in April, with the most current expansion in activity the weakest given that September 2021. Industrial and civil engineering do the job were being the most resilient segments, supported by Covid-19 recovery paying out and major infrastructure tasks respectively.

“Building corporations have constructed up powerful buy books considering the fact that the reopening of the United kingdom economic system, which led to one more spherical of rising employment in April and these project begins need to retain the sector in enlargement manner during the remainder of the next quarter.

“Even so, tender opportunities were being much less plentiful in April as growing inflation and larger borrowing expenditures started to chunk. As a result, longer-term progress projections have slumped from January’s peak, with enterprise optimism now the weakest given that September 2020.”

Duncan Brock, team director at the Chartered Institute of Procurement & Provide, said: “A slowdown in output development amongst builders in the United kingdom has highlighted a number of issues to be concerned about such as mounting prices, shortages and a hesitancy amongst buyers.

“New buy degrees rose at the slowest tempo given that the end of previous year. There had been fears about disrupted provides as 45% of offer chain supervisors claimed extended lead instances. To counteract some of these issues and with an eye on the long term, source chain administrators were being constructing stocks resulting in a further sharp increase in obtaining action.

“Inflation strike the optimum charge considering that September 2021, impacted on budgets and designed buyers think twice about committing. Job creation grew quickly to complete work in hand, jeopardizing above-inflating ability should new order advancement slow more. With the Financial institution of England confirming the interest fee as the maximum for 13 several years, the squeeze on company lending also led to a relatively gloomy outlook among builders for the calendar year ahead, with sentiment the most affordable due to the fact September 2020.”

Mark Robinson, chief government of general public sector procurement company Scape, reported: “After a buoyant initially quarter, a slowdown in sector output has felt pretty much inevitable. Cost raises and rising content fees are starting to factor into future paying for decisions at a time when general public organisations want the confidence to speed up tasks recognizing they will be delivered on time and to funds.

“Coupled with curiosity prices creeping up, companies across the source chain are most likely to see margins additional lessened in the coming months without having mindful job administration and engaged clientele. Any legislative aid mooted in the Queen’s Speech future week, such as the electrical power tactic invoice, are not likely to provide any rapid respite so open up dialogue among all parties will proceed to be vital for the rest of the yr at minimum.”

Received a story? E-mail [email protected]

[ad_2]

Resource connection