7 Steps to Retire in the Next 5-10 Years

[ad_1]

3. Slash Your Costs

No a single likes to hear this stage. But it’s important for two reasons.

To start with, if you are likely to conserve extra, that dollars needs to occur from somewhere. It could appear from additional side earnings (far more on that momentarily), but it also ordinarily that implies paying significantly less, so you can dedicate extra money to your retirement savings and investments. Consider dwelling hacking as the speediest single way to supercharge your cost savings charge.

The 2nd cause is somewhat more nuanced. Effective retirement is about reaching monetary independence, and fiscal independence needs that you exchange your active cash flow with passive earnings from investments.

The fewer revenue you expend in a offered calendar year, the easier it is to go over these charges with earnings from your investments.

If that seems like a uncomplicated idea, think about that each excess dollar you invest needs exponentially far more funds invested to address it. For simplicity, we’ll use the 4% Rule to illustrate this place.

The 4% Rule states that on common, you can count on withdrawing all around 4% of your nest egg each and every 12 months, to shell out your retirement charges, devoid of concern of functioning out of cash in your life time. That indicates you need to have 25 occasions as considerably income saved in your retirement portfolio as your yearly expending.

In other words, for every single thousand bucks you devote in a supplied year, you need to have $25,000 saved and invested.

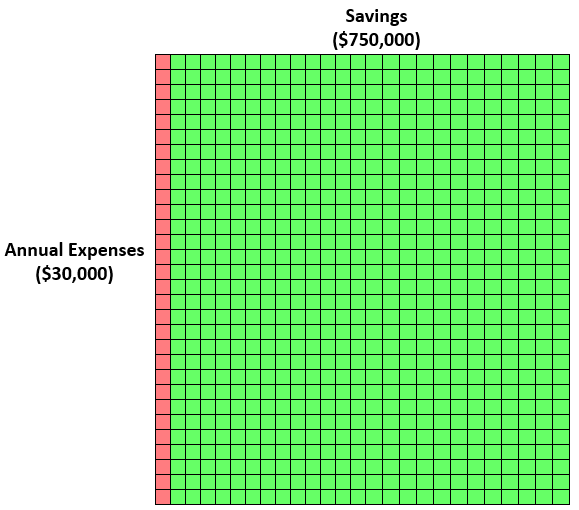

![]()

Like visuals? Zach from FourPillarFreedom illustrates this point with classy simplicity, applying small blocks. The red block earlier mentioned signifies $1,000 in shelling out in a calendar year. The environmentally friendly blocks are all the investments you are going to need to go over it.

If you want $30,000/12 months in passive money, that signifies a nest egg of $750,000. Here’s how that appears to be visually:

Get the idea? Every excess dollar multiplies your wanted nest egg exponentially, by 25 occasions.

Chris Mamula of Can I Retire But proposes a few concerns to assist you get there. “Could you downsize your residence or shift to a decrease cost of dwelling space? Could you go from a two-car or truck home to a just one vehicle domestic? Tips these types of as these could cost-free up cash tied up in homes and vehicles, when concurrently reducing ongoing expenses.”

4. Receive Much more Revenue Though You are Nonetheless Healthy & Operating

Your 40s and 50s are your peak earning many years. Meanwhile, your children are possibly older, so you’re not in zombie manner acquiring up three occasions every single evening to feed them.

You have connections. You have marketable expertise. In other text, you’re in a excellent position to press a small more durable and generate some extra cash.

I chatted with Michelle Schroeder-Gardner from Earning Feeling of Cents about her ideas on catching up on retirement investing. “My prime suggestion for anyone who is wanting to accelerate their retirement personal savings and investments would be to obtain approaches to make more cash.

“That could suggest having into rental true estate, finding a portion-time career, starting a facet business, achieving for that next promotion, and additional. I constantly like to point out that the ordinary individual watches over 30 several hours of Tv a week. That time could be utilised in direction of producing extra funds instead!”

When I asked Michelle if she had any a lot more thorough thoughts to aid people get their aspect hustle going, she didn’t disappoint. Here’s her listing of 75 Methods to Make Excess Funds, to help get people imaginative juices flowing!

And — spoiler alert! — 1 of people thoughts is, of system, buying rental qualities.

5. Rental Houses: How to Bend the 4% Rule

According the 4% Rule, you’d have to have $1,000,000 in retirement discounts in get to produce $40,000/year in passive earnings. That’s a tall buy for most of us.

But the 4% Rule was conceived based on equities and bonds. Equities are unstable, bonds are very low-yield… but what about residential rental attributes? A recent analyze analyzed all investment varieties above the previous 145 a long time, and uncovered that household rentals defeat out equities to present the most effective returns, especially when the economists adjusted for possibility and volatility.

Rental qualities are an earnings-focused investment, compared with most equities, which rely on appreciation in benefit for most of their returns. Employing rental qualities, investors can bend the 4% Rule, utilizing a lot less hard cash to generate additional income.

Rental qualities are an earnings-focused investment, compared with most equities, which rely on appreciation in benefit for most of their returns. Employing rental qualities, investors can bend the 4% Rule, utilizing a lot less hard cash to generate additional income.

Why? Very first, traders can use much a lot more leverage (other people’s cash) to invest in actual estate compared to other asset lessons. For a smaller down payment, traders can get a higher-price, higher-money-creating asset.

2nd, rental home returns are far extra predictable than equity returns. Just before paying for, Investors can correctly forecast a rental property’s dollars movement., by accounting for extended-expression average fees when calculating real estate money stream. (Use our totally free rental profits calculator to run the figures for any home.)

Rental houses protect versus inflation, way too: landlords can increase the lease each calendar year to preserve tempo with (or surpass) inflation. The identical can not be reported for bond or stock returns, which you have to modify for inflation.

Lastly, landlords have command over their returns. They can improve their house administration tactics, by automating hire selection, conducting periodic inspections, conducting in depth tenant screening, and many others. And if landlords want to charge drastically bigger rents, they can constantly enhance their property to command increased earnings.

[ad_2]

Supply hyperlink